16 Smart Money Moves to Take Before the End of the Year

October 17, 2025

The end of the year is a natural checkpoint for both individuals and small business owners. It’s when financial records should get reviewed, budgets get tightened, and people start thinking about how to position themselves for the year ahead. Making the right money moves during these final months doesn’t just clean up loose ends—it can also save on taxes, improve cash flow, and build a stronger foundation that can make the future brighter. Here are several smart strategies worth considering before it’s time to post the new calendar on the wall.

1. Review Retirement Contributions

One of the simplest yet most effective year-end strategies is to take stock of your retirement contributions. Individuals may want to check their 401(k) or IRA contributions to see if they’re on track to maximize tax-deferred savings. Small business owners should consider whether a SEP IRA or SIMPLE IRA contribution could both lower taxable income and provide long-term benefits for themselves and their employees.

2. Examine Charitable Giving

Before year’s end, those who are able should look at gifting cash, appreciated stock contributions, or other donations. Business owners can do the same. Charitable donations can offer substantial tax benefits, yes, but it’s also the right thing to do.

3. Check Estimated Tax Payments

Nothing upsets a new year’s toast like an unexpected tax bill. Reviewing estimated tax payments before December 31 can help ensure that individuals and businesses alike are in line with IRS requirements. Adjustments now can prevent penalties later, especially for those with fluctuating income or large year-end bonuses. Check in with your CPA to make this task easier.

4. Evaluate Business Expenses

Small business owners should scrutinize deductible expenses before the year closes. Purchases of equipment, software, or supplies made before December 31 may qualify for deductions—just make sure all receipts are kept in case they’re needed later. Business expense purchases should be made prior to ringing in the new year to count for spring tax season.

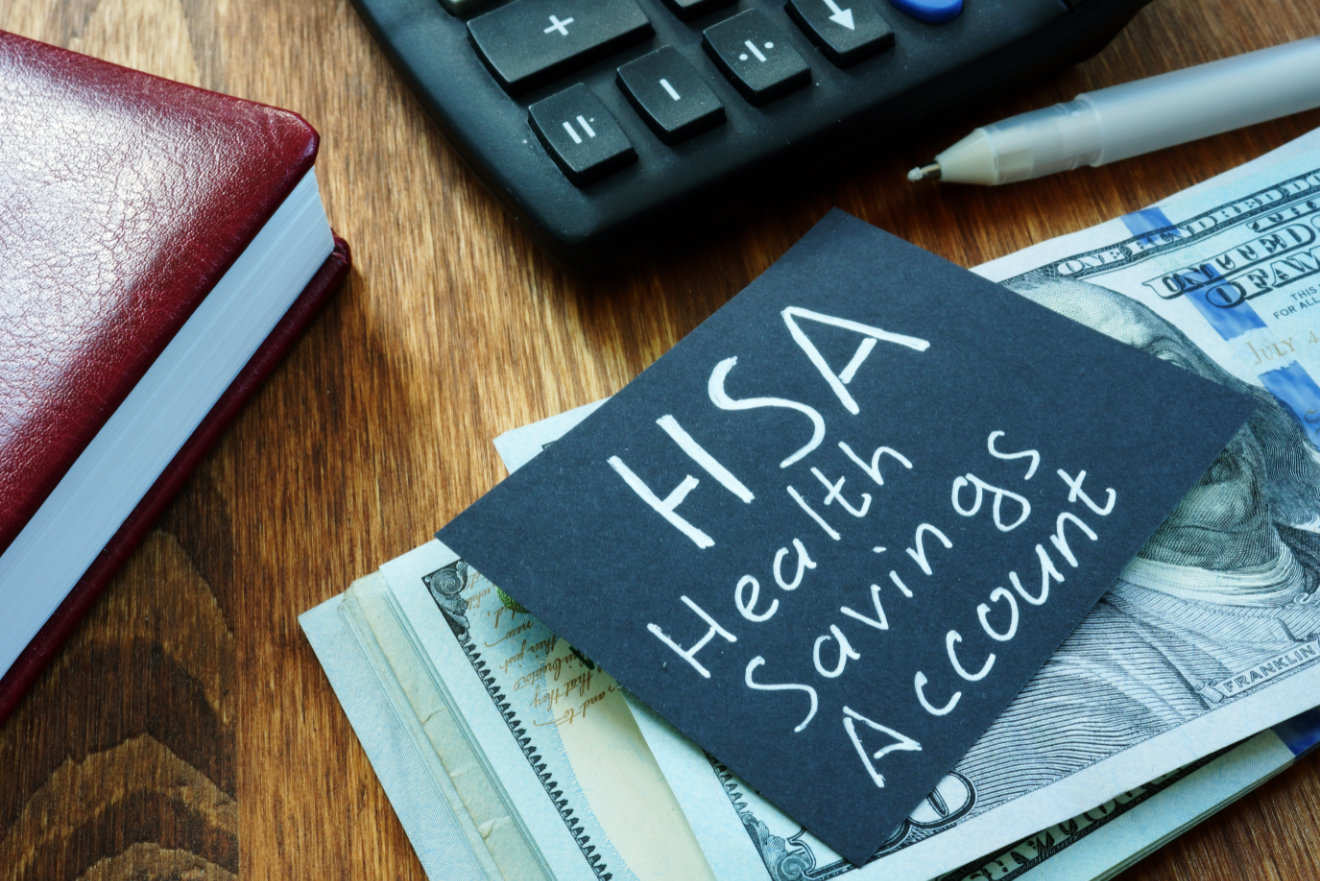

5. Review Health Savings Accounts

For people with high-deductible health plans, maximizing contributions to a Health Savings Account (HSA) can provide triple tax benefits: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified expenses remain untaxed. Reviewing balances and contributions before year-end ensures that the benefit is maximized.

6. Take a Fresh Look at Debt

Review outstanding balances on credit cards or loans and review the interest rates on that debt. Creating a repayment strategy, consolidating at a lower interest rate, or shifting balances to a no-interest introductory card can give a substantial boost to getting out of debt in the new year. Another idea is to contact debtors and ask for a lower interest rate.

7. Consider Timing of Income

For business owners and some individuals, income timing can affect tax liability. Deferring income into the next year or accelerating it into the current one, depending on anticipated tax brackets, can be an effective strategy. This requires a careful look at cash flow needs and consultation with a tax advisor, but the impact can be significant.

8. Revisit Insurance Coverage

Insurance policies should never be set-and-forget. A year-end review of life, health, auto, and property coverage ensures that protection still fits your needs. Business owners should pay special attention to commercial policies, making sure that liability and property limits reflect current operations and assets.

9. Plan for Education Costs

Families saving for education should review contributions to 529 plans or other education accounts before year-end. Many states provide tax benefits for contributions, and investing consistently ensures that compounding works in your favor. Business owners may also explore offering education benefits as part of employee compensation strategies.

10. Strengthen Emergency Savings

The last few years have underscored the importance of liquidity. A quick review of emergency savings ensures that individuals and businesses alike can weather unexpected expenses or downturns. Setting aside three to six months of essential expenses provides a cushion that keeps financial plans from unraveling during a crisis.

11. Analyze Investment Portfolios

Year-end is an ideal time to examine investments. Individuals may want to consider tax-loss harvesting, rebalancing asset allocations, or shifting investments to align with risk tolerance and future goals. Business owners should also review company investment accounts to ensure they reflect both risk management needs and long-term objectives.

12. Update Estate Planning Documents

Life changes—marriages, divorces, births, and deaths—can all impact estate planning needs. Year-end is the perfect time to revisit wills, trusts, and beneficiary designations. Individuals and business owners alike benefit from keeping these documents up-to-date to avoid legal complications later.

13. Look Into Year-End Bonuses

For business owners, offering year-end bonuses can reward employees while potentially reducing taxable income. Structuring bonuses effectively requires careful planning but can provide motivational benefits that carry into the next year. Individuals expecting bonuses should think about how to allocate them—whether toward savings, debt reduction, or future investments.

14. Double-Check Recordkeeping

Good records make tax season easier. Year-end provides an opportunity to organize receipts, update bookkeeping, and reconcile accounts. For small businesses, strong records not only simplify tax filings but also provide a clearer picture of profitability and opportunities for growth.

15. Think About Next Year’s Goals

While reviewing current-year strategies is important, setting intentions for the next year matters just as much. Whether it’s saving for a down payment, expanding a business, or simply creating a more predictable budget, year-end reflection creates a roadmap for success.

16. Taking Advantage of the Calendar

The end of the year isn’t just another date on the calendar—it’s an opportunity. By reviewing contributions, tightening expenses, and aligning strategies with long-term goals, both individuals and small business owners can position themselves for greater financial stability. Taking these steps now means starting the new year not with uncertainty but with confidence, knowing that you’ve done the work to put your money to its best use.

In the end, year-end planning isn’t about rushing through a checklist. It’s about slowing down, reviewing what matters most, and making choices that set you up for a stronger financial tomorrow. With the right steps taken now, the year ahead can bring clarity, growth, and the peace of mind that comes with being prepared.

by Kate Supino